The World Bank Doing Business is a tool that measures regulations that enhance business activity and those that constrain it and it also measures regulatory quality and efficiency.

There has been a recognition that regional integration alone is not enough to spur growth. The EAC needs an investment climate—including a business regulatory environment—that is well suited to scaling up trade and investment and can act as a catalyst to modernize the regional economy. Despite the reform efforts of all 5 member economies, the EAC’s average ranking on the ease of doing business has remained fairly constant over the past 4 years, at around 117 and in fact comparing the 2010 Doing Business performance to 2013, the EAC has seemingly not registered much of an improvement. This is a clear indication that critical obstacles to entrepreneurial activity remain and that economies in other regions have picked up the pace in improving business regulation. Improving the investment climate in the EAC is therefore an essential ingredient for successful integration—the foundation for expanding business activity, boosting competitiveness, spurring growth and, ultimately, supporting human development.

The development of regional strategies and institutional frameworks that connect and streamline national reform programs is an indispensable condition for a well-functioning common market that can attract foreign investment. A lack of coordination among member countries and the implementation of “isolated” national reforms—which often focus on short-term gains and fail to consider the impact on the region—can hinder progress in fully implementing the common market. Conversely, continual exchange among different authorities across countries, the implementation of an agreed-on regional reform agenda and a focus on common goals and objectives create synergies and help the region as a whole to improve its investment climate.

Fostering economic growth by tapping the potential of the private sector is among the main objectives of the fourth EAC development strategy. In addition to increasing institutional coordination, other important steps to achieve this objective are better integrating small and medium-size enterprises into the financial sector and creating business-friendly administrative structures and tax regimes. Additional challenges are to ensure the availability of reliable data and statistics and to implement credible surveillance and enforcement mechanisms.

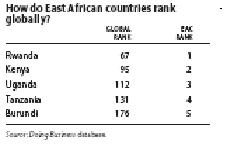

The EAC economies have an average ranking on the ease of doing business of 117 (among 185 economies globally). But there is great variation among them—from Rwanda at 52 in the global ranking to Burundi at 159. This wide variation in business regulations is among the issues that the EAC needs to tackle to achieve the desired level of integration. While the regional average ranking is less than ideal, if a hypothetical EAC economy were to adopt the region’s best regulatory practices in each area measured by Doing Business, it would stand at 26 in the global ranking on the ease of doing business. Burundi was among the world’s most active economies in implementing regulatory reforms in 2011/12. It implemented policy changes in 4 areas measured by Doing Business: starting a business, dealing with construction permits, registering property and trading across borders.

One area where the EAC shows strong performance is business start-up. To start a business in the EAC requires only 8 procedures and 20 days on average. As such the EAC’s average ranking on the ease of starting a business is 84, higher than those of other regional blocs in Africa—104 for the Southern African Development Community (SADC), 110 for the Common Market for Eastern and Southern Africa (COMESA) and 127 for the Economic Community of West African States (ECOWAS)

The 2013 Doing Business Report on the EAC can be downloaded here.